Advancing thinking when calculating LTV

When it comes to LTV, it's important to consider time value of money and margins rather than revenue.

Update: Thanks to those that have pre-ordered my book. I’m in the process of working with a copy editor and revising the manuscript. For those that want a sneak peak, Chapter 4: Building better relationships, submit 5 referrals to my Substack.

In my article, “Understanding important direct to consumer metrics”, I discussed calculating LTV (Lifetime Value).

One reason LTV is important is that in many cases, the average CAC is significantly higher than the AOV. Thus, the only way to make money back is if over time, that customer buys something again the next month and so on. Over time, the LTV will increase, hopefully, above the CAC.

But real-life PM is always a bit more complicated than the simple example I used in my prior post. Take the following. Which is better?

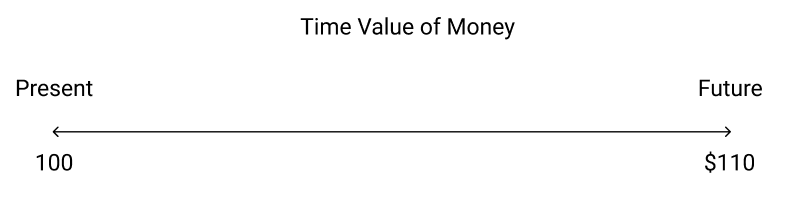

A customer who spends $100 dollars one time and never buys again

A customer who spends $55 twice, over two time periods

If you answered it depends…you’re obviously schooled in the time value of money and discounting.

When to start thinking about discounting?

The basic LTV calculation is simple. You only need a few pieces of information because this LTV calculation is the total revenue of an average customer. So, you only need to know:

How much an average customer spends via average order value (AOV)

What percentage of customers return and buy something again via retention rates as a percentage

With the basic LTV, you can compare against the customer acquisition cost (CAC) to understand if the LTV is greater than the marketing dollars spent to acquire a paid customer.

But notice two small issues:

CAC is money spent early, at period 0. LTV is the sum of a customer’s spending over time (period 0, 1, 2, … n). The time periods don’t align because you get revenue later or “over time”.

LTV is calculated as the sum of the customer’s spending (i.e., company’s total revenue). But revenue isn’t profit and CAC is only a portion of the company’s costs. What about the cost of goods sold (COGS) or cost of sales (COS)? The LTV could be higher than CAC and the company could still have negative margins/profits.

Underlying these two issues are two unspoken assumptions PM face in most early stage startups:

Worrying about “time periods not aligning” between when money is spent (i.e., CAC) vs. revenue over time (i.e., LTV) isn’t important because it’s not a common way investors look at when companies raise equity or debt. Furthermore, determining the discount rate to discount your cumulative customer’s revenue is unnecessarily difficult and subjective, rendering it useless.

COGS or COS will decrease over time whether due to economies of scale or operational process improvements. Thus, understanding and reducing such costs too early isn’t important if the company doesn’t yet have product-market-fit (i.e., clear demand shown by low CAC).

There’s some general truth to the above and worrying about both are too complex for pre-Series B startups. But as the company matures, understanding costs, margins, and discount rates are important factors because that’s how public companies are compared and evaluated. Given that many startups hope to go public, how should PMs start advancing LTV calculations?

How to advance LTV calculations?

Start by looking at the stage of your company. If you’re before Series B, I’d argue you can skip. Otherwise, read on.

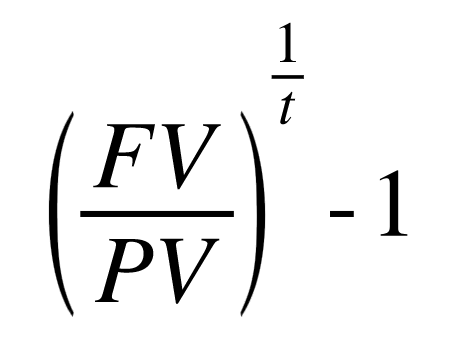

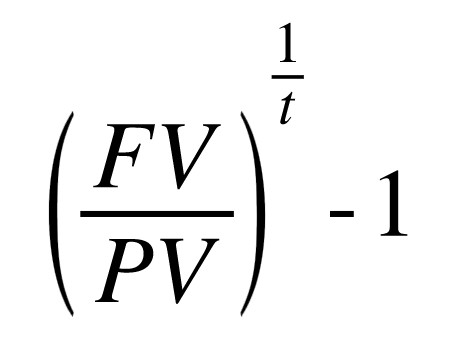

Determine your discount rate by taking the company’s current valuation and it’s targeted valuation for the next fundraising round. Identify the time period it’ll take to reach this round.

Calculate the discount rate.

[(Future Valuation / Present Valuation)^(1 / time period in years)] -1

Calculate the contributing margins = AOV - COS - average sales discount

Calculate the retention rate using the same duration/time period used in the discount rate calculation.

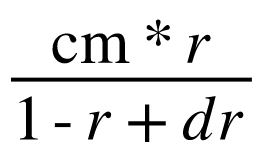

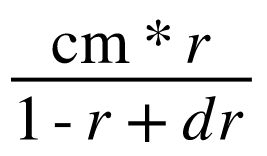

Calculate the discounted, contributing margin LTV.

(contributing margins * retention rate) / (1 - retention rate + discount rate)

This discounted, contributing margin LTV is the profit each customer contributes to the bottom line.

A few final comments to make it even more practical

The discount rate can be greater than 100% for startups because of the high expectations in growing valuation. Discount rate will decrease over subsequent rounds as valuation growth also declines in absolute percentages.

Many PMs at startups don’t know COGS, COS, and sales discounts. Thus, it can be difficult or impossible to calculate margins. If this is the case and you can’t get the data, use AOV instead of contributing margin in the above equation. But note that the LTV is a revenue number, not a margin based number.

There are different margins (e.g., product, gross, or contribution). While it matters, it also doesn’t. Use the one that your company is comfortable with as a start.

Special thanks to Clarence Lee, Professor @ Cornell, for the chat that sparked this post and his SPMI course materials.

Additional Reading:

The difference between contribution margin and gross margin (you might see me using the two terms CM/GM interchangeably in the last two articles. There are differences, but I’m using them interchangeably.)